Running an online store means dealing with payments every day. And at some point, you’ll likely run into a PayPal chargeback. It can feel confusing – money disappears from your account, and you’re not sure why or what to do next.

This guide breaks it all down. You’ll learn what is PayPal chargeback, how it’s different from a dispute or refund, how much it costs, how long it takes, and what you can do about it – whether you’re a merchant or a buyer.

What Is PayPal Chargeback?

PayPal chargeback is a situation that happens when a buyer contacts their bank or card issuer – not PayPal – to dispute a charge. The buyer asks their bank to reverse the payment, and the bank takes control of the process from there.

Here’s the key thing to understand: PayPal doesn’t decide the outcome of a chargeback. The card issuer does. PayPal’s role is to notify you, place a hold on the funds, collect your evidence, and pass it along to the card issuer on your behalf.

How Does a PayPal Chargeback Work?

Here are step by step how PayPal chargebacks work:

- The buyer contacts their bank and files a chargeback.

- The bank withdraws the funds from PayPal and places a hold on the seller’s account.

- PayPal notifies the seller and asks for evidence to contest the chargeback.

- The seller chooses to either accept the loss or fight it by submitting evidence through the Resolution Center.

- PayPal forwards the evidence to the card issuer.

- The card issuer reviews everything and makes the final call. If the seller wins, funds are returned. If the buyer wins, the money goes back to the buyer.

This process is different from a PayPal dispute, which is handled entirely inside PayPal’s platform. More on that below.

Why Do PayPal Chargebacks Happen?

In reality, the list below is the root cause of every kind of customer dissatisfaction. When these problems first come up, customers usually open a Dispute with you on PayPal to try and sort things out. But if you ignore them, give a weak response, or take too long to reply, that Dispute can quickly escalate into a Chargeback through their bank.

Let’s go through the most common reasons so you can stop them while they’re still just a Dispute, before they turn into something bigger:

“I Never Got My Package”

The buyer says their order never arrived. This is the most common reason, by far.

The good news? It’s also the easiest to win. If you have a tracking number that shows the package was delivered to the right address, you’ve got solid proof on your side.

“It’s Not What I Ordered”

The buyer says the product doesn’t match what was in your store. Wrong color, wrong size, looks cheaper than the photos, that kind of thing.

This one’s harder to win because it’s their word against your listing. The fix is simple, though: use real photos, write clear descriptions, and don’t oversell. The fewer surprises buyers get, the fewer chargebacks you’ll see.

“I Didn’t Buy This”

For this credit card fraud reason, buyers usually skip the Dispute step on PayPal and go straight to a Chargeback with their bank the moment they spot the charge on their statement or notice a balance change.

Card issuers take these very seriously, so they’re tough to fight unless you have strong proof, like a delivery to the cardholder’s confirmed address.

“I Was Charged Twice”

The buyer thinks they were billed for the same order twice. Sometimes it’s a real glitch. Sometimes the buyer just doesn’t recognize a second order on their bank statement.

A quick reply with the order details usually clears this up before it becomes a real problem.

“I Canceled My Subscription But Got Charged Again”

This one’s all about recurring payments. The buyer either forgot they signed up, didn’t notice the auto-renewal, or canceled and got charged anyway.

Send a reminder email before each renewal. Make canceling easy. That alone prevents most of these.

“You Promised a Refund and Never Sent It”

The buyer is waiting for a refund and gives up. They go to their bank instead.

Always send refunds through PayPal, not Venmo, not a bank transfer, not anywhere else. That way, there’s a clear record tied to the original payment.

What Is PayPal Chargeback Fraud?

Not every chargeback is honest. Some buyers file chargebacks even when they got their order, it was delivered fine, and nothing went wrong. They just want their money back and keep the product.

This is called chargeback fraud. People also call it “friendly fraud,” which is a funny name because there’s nothing friendly about it.

How It Works

A buyer places an order. The package arrives. A week later, they call their bank and say something like:

- “I never got it.”

- “I didn’t buy this.”

- “This isn’t what I ordered.”

The bank usually sides with the buyer, especially on smaller orders. The buyer keeps the product. You lose the money and pay the chargeback fee.

Why It’s Getting Worse

Chargeback fraud is growing fast. Here’s why:

- It’s easy. Buyers can file from their phone in two minutes.

- They usually win. Banks tend to trust the cardholder.

- There’s no real downside for the buyer. Even if they get caught, the worst case is the bank closes their account.

It’s worse in things like clothing, digital products, and pricey items. Anything a buyer might want to “keep and complain about.”

How to Spot It

Watch for these warning signs:

- The buyer never emailed or messaged you before filing

- Tracking clearly shows the package was delivered to their address

- They’ve filed chargebacks at other stores too

- Their story doesn’t match the facts (like claiming “didn’t arrive” when it was signed for at their door)

How to Fight Back

If you think it’s friendly fraud, here’s what helps:

- Send every piece of proof you’ve got. Tracking, delivery confirmation, signature, even screenshots of any messages.

- Point out anything that doesn’t add up. If their story has holes, show them.

- Save all your customer messages. Proof of contact means a lot.

- Follow PayPal’s eligibility rules so Seller Protection kicks in automatically. As long as your transaction qualifies (ship to the address on file, use tracked delivery, keep proof of shipment), PayPal applies Seller Protection on its own. That can save you from “didn’t arrive” and “unauthorized” claims without you lifting a finger.

Here’s the honest truth: even with great evidence, you won’t win every time. The bank makes the call, and they don’t always play fair. But the more proof you send, the better your chances.

PayPal Chargeback vs PayPal Dispute vs Refund

One of the most common points of confusion is the difference between these three terms. They all involve getting money back, but they work very differently.

|

Chargeback |

PayPal Dispute / Claim |

Refund |

| Who starts it |

Buyer (with their bank/card issuer) |

Buyer (or seller) in PayPal’s Resolution Center |

Seller |

| Who decides |

Card issuer |

PayPal (once escalated to a claim) |

Seller |

| Funds held? |

Yes, while the case is open |

Yes, during the dispute/claim |

No hold – money is returned directly |

| Deadlines |

Buyer: ~180 days; Seller response: ~10 days |

Buyer must escalate within 20 days; Seller: ~10 days to respond |

Sellers can issue refunds within 180 days |

| Fees |

Chargeback fee may apply |

Dispute fee may apply |

No fee to refund, but receiving fees aren’t returned |

PayPal Chargeback Fee: How Much Does It Cost?

Fees are one of the biggest concerns for merchants dealing with chargebacks. PayPal charges two types of fees you need to know about: the chargeback fee and the dispute fee. They’re not the same thing.

Chargeback Fee

When a buyer files a chargeback with their card issuer, PayPal gets charged by the card network. PayPal then passes that cost to the seller.

For US merchants, the chargeback fee is $20 USD. This fee applies to certain card chargebacks that are not processed through a buyer’s PayPal account or guest checkout.

Important: PayPal charges this fee regardless of whether the buyer wins the chargeback or not.

Dispute Fee

The dispute fee is separate and applies to cases that go through a buyer’s PayPal account or guest checkout – including disputes, some chargebacks, and bank reversals.

There are two tiers:

- Standard Dispute Fee: $15 USD

- High Volume Dispute Fee: $30 USD

Source: PayPal’s Dispute Fees

You’re placed in the High Volume tier if your dispute rate is 1.5% or higher and you’ve had more than 100 sales in the prior three full calendar months.

When Are Fees Waived or Reimbursed?

You won’t always be charged. PayPal waives or reimburses fees in certain situations:

- The case is resolved before escalation

- The transaction is covered by PayPal Seller Protection

- The case involves an unauthorized transaction claim filed directly with PayPal

- The claim amount is very small

- PayPal or the card issuer decides in the seller’s favor

One important distinction: if you win an appeal, PayPal reimburses the Standard Dispute Fee ($15). The High Volume Dispute Fee ($30) is not reimbursed, regardless of outcome, because it’s based on your overall dispute rate – not the result of any single case.

What About Chargeback Protection?

PayPal also offers Chargeback Protection as an optional add-on for eligible business accounts using Advanced Debit and Credit Card checkout (ACDC). If you’re eligible, it can waive the chargeback fee and remove the hold on your funds for certain dispute types – specifically “unauthorized” or “item not received” chargebacks.

Keep in mind: this product isn’t available to all merchants, and it has loss caps and exclusions. Check your PayPal account to see if you qualify.

Note: Fee amounts and availability vary by country. The figures above are US examples. Always check PayPal’s fees page and your local user agreement for the most accurate information.

How Long Does PayPal Chargeback Take?

Timing is everything when it comes to chargebacks. There are three separate clocks running at the same time – and missing any one of them can cost you.

For Buyer

Buyers can typically file a chargeback within 180 days of the transaction date, according to PayPal’s Help Center. PayPal also notes that buyers can file “180 days or more” after an order, depending on the card issuer’s own rules.

For context, many card networks typically require buyers to file within 60 to 120 days of the transaction – but this varies by issuer and region.

For Seller

Once PayPal notifies you of a chargeback, you generally have about 10 days to respond with your evidence.

If you’re in the High Volume Dispute Fee tier, that window can shrink to just 3 days. This is a critical detail that many sellers miss.

Don’t wait. As soon as you receive a chargeback notification, open the Resolution Center and start gathering your documentation.

How Long Until a Decision?

This part takes the longest. Here’s a realistic breakdown:

- PayPal typically takes about 30 days to dispute a chargeback on your behalf.

- The card issuer then takes its own time to review – often up to 75 days.

- Total resolution is commonly described as “a few weeks,” but it can stretch to 75 days or more.

Plan your cash flow accordingly. Funds are held during this entire period.

| Stage |

Who’s Responsible |

Typical Timeframe |

| Buyer files chargeback |

Buyer / card issuer |

Any time within ~180 days of transaction |

| PayPal notifies seller; funds held |

PayPal |

Shortly after bank notifies PayPal |

| Seller submits evidence |

Seller |

Within ~10 days (3 days for High Volume tier) |

| PayPal disputes the chargeback |

PayPal |

~30 days |

| Card issuer makes final decision |

Card issuer |

Up to ~75 days |

| Funds returned or refunded |

PayPal |

After issuer decision |

PayPal Chargeback Policy and Seller Protection

Understanding PayPal’s Seller Protection program is one of the most valuable things you can do as a merchant. It can cover your losses and even waive the chargeback fee – if you meet the requirements. On average, merchants win around 20–30% of chargeback disputes, but this rate varies by industry and dispute type – and can improve significantly when you submit strong evidence like delivery confirmation and customer communication records.

What Is PayPal Seller Protection?

Seller Protection is PayPal’s program that shields eligible merchants from certain types of chargebacks. If your transaction qualifies, PayPal may cover the reversed amount and waive the chargeback fee – even if the buyer wins.

The key phrase here is “if your transaction qualifies.” Eligibility depends on following PayPal’s specific requirements carefully.

Eligibility Requirements

To qualify for Seller Protection, you generally need to:

- Ship to the address on file in the PayPal transaction details

- Provide proof of shipment or proof of delivery with a valid tracking number, shipping date, and “delivered” status

- For unauthorized transaction claims: ship the item no later than two days after PayPal notifies you of the dispute or reversal – this is a strict deadline that catches many sellers off guard

- For digital goods: provide “compelling evidence” of delivery or access (system logs, access timestamps, delivery confirmation)

What Evidence Should You Submit?

The evidence you need depends on the reason for the chargeback:

For physical goods:

- Tracking number with carrier confirmation of delivery

- Recipient address matching the PayPal transaction

- Proof of refund (if you’ve already issued one)

- Your return/cancellation policy

For digital goods:

- System records showing electronic delivery

- Access logs with timestamps

- IP address or login records tied to the buyer

General tip: Submit everything in one go. PayPal may not give you a second chance to add evidence after your initial submission.

Can You Appeal a PayPal Chargeback Decision?

It depends on the type of decision:

- PayPal claim decisions can be appealed – but only if you have new information. You must appeal within 10 days of the case closing in the Resolution Center.

- Card issuer decisions on chargebacks cannot be appealed through PayPal. The issuer has final say.

How to Respond to a PayPal Chargeback

If you get hit with a chargeback, here’s exactly what to do:

Step 1: Open the Resolution Center immediately.

Read the chargeback reason carefully. The reason code tells you what the buyer is claiming – and that determines what evidence you need.

Step 2: Decide whether to contest or accept.

If you’re confident you can prove your case, contest it. If the buyer has a valid point, accepting the chargeback is often faster and cheaper.

Step 3: Gather your evidence.

Based on the chargeback reason, pull together your proof of shipment, delivery confirmation, communications with the buyer, and your return policy.

Step 4: Submit everything before the deadline.

You have about 10 days (sometimes 3). Don’t delay. Submit all your documentation at once – organized and clearly labeled.

Step 5: Monitor the case. Chargebacks can take weeks or months to resolve. Keep an eye on the hold on your funds and track the case status in PayPal.

How to Prevent PayPal Chargebacks

The best chargeback is the one that never happens. Here’s what you can do to reduce them:

- Be easy to reach. Many chargebacks happen because buyers can’t get a response from the seller. Make your contact information easy to find and reply quickly.

- Set clear expectations. Accurate product descriptions, realistic shipping timelines, and honest photos go a long way. When buyers know what to expect, they’re less likely to dispute.

- Communicate proactively. If there’s a delay, tell the buyer before they notice. A short “your order is on its way” message can prevent a dispute entirely.

- Issue refunds through PayPal. If you need to refund a buyer, use the refund link inside the Resolution Center – not outside PayPal. Refunds issued outside may not count toward Seller Protection.

- Track everything. Always use shipping options with tracking. No tracking number = no proof of delivery = no Seller Protection.

- Resolve disputes early. If a buyer opens a dispute, try to resolve it directly before it escalates into a formal claim or chargeback. Early resolution avoids fees and keeps your dispute rate low.

>>> Learn More: How to Avoid Chargebacks on PayPal: 6 Proven Ways to Protect Your Business Profits

Stop Losing Money to Chargebacks – This Tool Does the Heavy Lifting

Here’s a hard truth most merchants learn too late: a chargeback isn’t just a payment reversal. It’s a signal to PayPal that something went wrong. Too many of them, and your funds get held longer, your dispute fees go up, and your account trust takes a hit.

The root cause? Missing or unverified tracking information. When PayPal can’t confirm that an order was shipped and delivered, disputes are easier for buyers to win – and harder for you to fight. You end up spending hours gathering tracking numbers, uploading evidence manually, and waiting weeks for PayPal to release your funds.

And if you’re managing dozens or hundreds of orders a month, doing this manually isn’t just inefficient. It’s a liability.

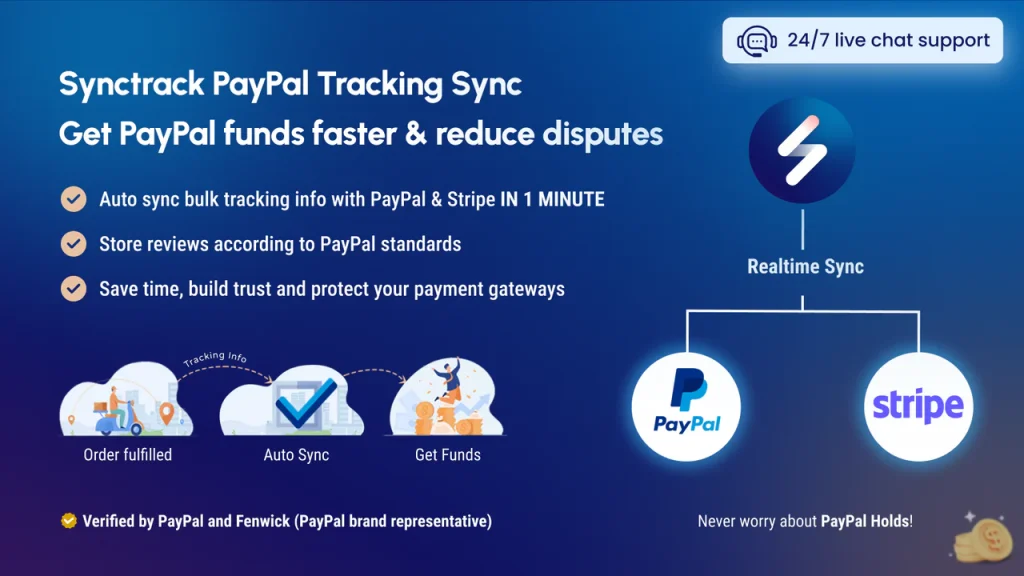

That’s where Synctrack PayPal Tracking Sync comes in.

Synctrack is a Shopify app that automatically syncs your order tracking information to PayPal and Stripe in real time – no manual uploads, no missed orders. The moment a package ships, PayPal gets the tracking number. That means PayPal can verify the transaction faster, release your funds sooner, and flag your account as low-risk.

Here’s what Synctrack does for your store:

- Auto-syncs tracking to PayPal and Stripe as soon as orders are fulfilled – no manual work required

- Gets your funds within 1–3 days by giving PayPal verified shipping data upfront

- Reduces disputes and chargebacks by keeping buyers informed with valid tracking information

- Strengthens your PayPal Seller Protection by adding tracking transparency to every transaction

- Syncs orders from Shopify, Facebook, and Instagram sales channels in one place

- Auto-matches courier names with PayPal-supported carriers to avoid verification delays

- Manages multiple PayPal accounts and Shopify stores from a single dashboard

If you’re serious about reducing chargebacks, the most effective thing you can do is make sure PayPal always has verified tracking on every order. Synctrack makes that automatic.

PayPal Chargeback FAQs

What is a PayPal chargeback and how does it work?

A PayPal chargeback is when a buyer contacts their bank or card issuer to dispute a charge. The bank withdraws the funds from PayPal, which then holds the seller’s money while the case is reviewed. PayPal collects the seller’s evidence and sends it to the card issuer, who makes the final decision.

What’s the difference between a PayPal chargeback and a PayPal dispute?

A dispute is opened inside PayPal’s Resolution Center and decided by PayPal. A chargeback is filed with the buyer’s bank or card issuer and decided by the card issuer. Disputes are generally faster and less costly for both sides.

How much is the PayPal chargeback fee?

For US merchants, PayPal charges a $20 chargeback fee for card chargebacks not processed through a PayPal account. Separately, a dispute fee of $15 (Standard) or $30 (High Volume) may apply for cases processed through PayPal or guest checkout. Fees vary by country.

Do I get the chargeback fee back if I win?

If you win and you were charged the Standard Dispute Fee ($15), PayPal reimburses it. The High Volume Dispute Fee ($30) is not reimbursed, even if you win.

How long does a PayPal chargeback take to resolve?

Total resolution can take anywhere from a few weeks to 75 days or more. PayPal typically takes around 30 days to dispute the chargeback, and the card issuer can take up to 75 days to make a final decision.

How long does a buyer have to file a PayPal chargeback?

Buyers can typically file a chargeback within 180 days of the transaction date. However, the actual deadline depends on the card issuer’s own rules, which can vary.

How long does a seller have to respond to a PayPal chargeback?

Sellers generally have about 10 days to respond. If you’re in the High Volume Dispute Fee tier (dispute rate ≥ 1.5%), you may only have 3 days.

Final Thoughts

A PayPal chargeback can feel overwhelming the first time you deal with one. But once you understand how the process works – who’s involved, what the deadlines are, and what evidence matters – you’re in a much stronger position to handle it.

The most important things to remember:

- Chargebacks are decided by the card issuer, not PayPal

- You have around 10 days to respond (sometimes less)

- Seller Protection can cover your losses if you meet the requirements

- Prevention is always cheaper than fighting a chargeback after the fact

- Fees add up fast – a $20 chargeback fee plus a $15–$30 dispute fee can turn a small transaction into a significant loss

Stay proactive, keep your documentation organized, and make it easy for buyers to reach you. Those three habits alone will reduce your chargeback risk significantly.